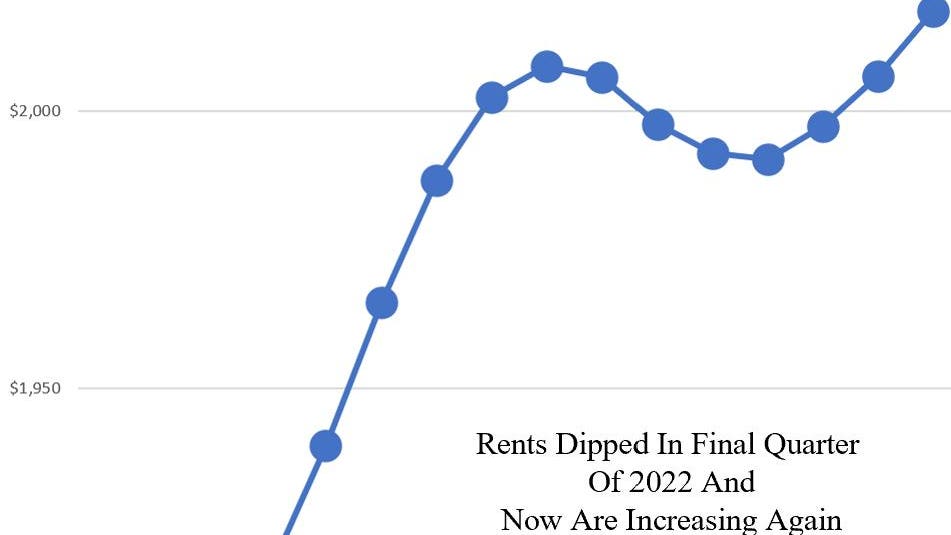

Real estate investors and developers have been concerned in recent months about the direction of rents. Rents on multifamily apartments as well as rental homes and townhomes peaked after the massive and clearly-unsustainable rates of increase of the prior two or three years, underwent a short correction, and now appear to be rising again. This raises the question of whether the correction has already played itself out, or whether a second dip lies ahead. Either way, it is fascinating to see the upswing, which is occurring ahead of the normally strong summer season (February, March, and April all showed increases).

The ZORI (”Zillow Observed Rent Index”), graphed above, is a valuable measure of residential rents that leverages extensive rental data from multiple sources, providing insights into median rent values across various geographic areas. Its methodology factors out the effects of seasonality and property age, quality, and composition (by measuring the rent at a particular property at two periods of time), ensuring a more accurate representation of rent changes. The data through April are shown here, and our channel checks indicate that the upswing continued in May.

Also, the CoreLogic single-family rent index has bottomed out, as I have discussed in past articles, suggesting a return to positive rent growth for single-family rentals as well.

The Significance of Consecutive Rent Increases

A series of consecutive increases in rents suggests a sustained upward trajectory in rental prices, rising by 1.3% in three months following a very slight pullback in the final months of 2022. The outlook is for modest rent growth (3%-5%) as opposed to the double-digit rates of increase of the prior 24 months.

The renewed up-trend may be indicative of several favorable factors of interest to investors in residential real estate:

Growing Demand: The rent hikes reflect increased demand for rental properties, and we can see strong absorption happening so far in 2023, keeping up with new supply. It will be important to watch the balance between completions (ready to increase in the second half), and demand as we continue into the fall and winter.

Limited Supply: In some areas, the supply of rental properties struggles to keep up with demand, particularly in the realm of new rental single-family homes, cottages, and townhomes. Supply constraints can stem from regulatory restrictions, a lack of available land, or delays in new construction. As rental demand outpaces supply, investors may find themselves in a position of strength, with the ability to command higher rents and increase their overall return on investment.

Improved Sentiment: Consecutive rent increases correlate with positive economic conditions, such as job growth, rising incomes, and sentiment about job security. These factors can lead to increased household formation and a greater number of people seeking rental accommodations.

Limited Affordability: Escalating home prices and higher mortgage rates push aspiring homeowners towards the rental market. As homeownership becomes less accessible for some individuals or families, rental demand intensifies. Investors can leverage this situation by offering quality rental properties that cater to the needs of young families who are unable to buy a home but who want a place with a yard.

Reinforcing the Investment Thesis

Our analysis suggests that the weakness that took hold in the rental market last fall stemmed from a surge of headlines and worry about an impending recession. The

recession may still come, but it looks as if some of the effects on rents came early. People who were living with roommates or relatives and who were considering moving out and getting a place of their own hesitated to do so, and that showed up as slower leasing paces at new built-for-rent developments and new apartment buildings, and as lower effective rents. Now, it appears that some of the people who delayed their plans are looking around and realizing that they still feel secure in their jobs and are moving ahead with their plans to get their own place. Compounding this resurgence of demand is the large number of millennials who are starting to have kids, and thereby outgrowing apartment living. This is particularly stimulating demand for single-family rentals and townhome rentals.

Renters’ incomes are growing faster than the incomes of the population as a whole, partly reflecting millennials advancing in their careers. This allows further room for rent escalations in the years ahead. Renters of Class-A properties only spend about 23% of their income on rent (per research from RealPage), which is below the 30%-33% cutoff that is considered too high.

Conclusion

Investors who closely monitor and analyze these trends have the opportunity to capitalize on changes in the rental market. By seeing the inflection points as soon as they occur, investors can position themselves for success.

To say that we had a “correction” and that it is now “over” is taking things too far, as the dip that occurred last fall was minor compared with the prior runup. It was not a “correction” so much as a response to a suddenly more sober view of the economy. It is worth taking notice however that rents appear to be holding up better than they had been, and will likely continue to do so as long as renters’ incomes do not encounter a massive disruption.

The forecast from Hunter Housing Economics calls for modest and sustainable increases in rents (particularly for single-family homes and townhomes/duplexes, as well as cottages) this summer and into the fall, but warns that a seasonally-normal dip is likely next winter, followed by further rent growth in 2024. A deeper-than-expected recession could further depress rents on a short-term basis, but such an event would also likely drive a number of would-be buyers back into the rental market.

Read the full article here