“ The U.S. stock market is likely to struggle in coming weeks. ”

Contrarians are betting that the U.S. stock market will struggle in the month of April.

That’s because of the widespread narrative that April is the best month of the year for the stock market. That premise is either highly misleading or outright wrong, depending on how you view the data. This false narrative is helping to create the “slope of hope” that is the opposite of the “Wall of Worry” that markets like to climb.

As examples of this narrative, consider a recent communication to clients from Jeffrey Hirsch, editor of the Stock Trader’s Almanac. He writes that April is “the #1 performing DJIA month of the year since 1950.” Or take Matthew Carr, editor of First Bar with Matthew Carr website. He analyzed the past three decades and found that April has the highest probability of success of any month. Concluding that April is “routinely the best month of the year for stocks,” Carr refers to the month as “Awesome April.”

I don’t mean to pick on Hirsch and Carr, who are not alone among the newsletter editors I monitor in believing the seasonal tendencies favor a strong April. But to one extent or another these newsletter editors focus on just some of the historical data while ignoring other parts. It’s a statistical no-no to not focus on all available data.

Average April

When you analyze the Dow Jones Industrial Average

DJIA,

as far back in history as the data will allow, April is unexceptional. Since the Dow’s creation in 1896, April’s average return is no different than those of the other 11 months at the 95% confidence level that statisticians use when determining if a pattern is genuine. Furthermore, the stock market’s probability of success in April is unremarkable, at 60%. That compares to 58% for the other 11 months of the calendar.

It’s a sure sign that investors are being motivated by sentiment rather than fundamentals when they base their bullishness on historical arguments that are so flimsy. Contrarians believe it’s an especially good idea to bet against the consensus when investors are ignoring the obvious holes in their arguments.

To measure the consensus, I focus on the average recommended equity exposure level among several dozen short-term stock market timers. The chart above plots this average among timers who focus on the Nasdaq Composite

COMP,

in particular, as measured by the Hulbert Nasdaq Newsletter Sentiment index (HNNSI). Because Nasdaq-focused timers are quick to shift their recommended exposure levels when there’s even a hint of a mood change on Wall Street, the HNNSI is my most sensitive measure of market sentiment.

As you can see, the HNNSI has soared over the last two weeks and is now within shouting distance of being in the top decile of the distribution of daily readings since 2000. This highest decile is shaded in the chart; in prior columns I have used this decile to indicate excessive bullishness. While the contrarian-based odds of April being a down month therefore aren’t as strong as they would be if the HNNSI were in that highest decile, its current above-average level suggests that the U.S. stock market is likely to struggle in coming weeks.

At a minimum, there is no sign that the month will be “Awesome April.”

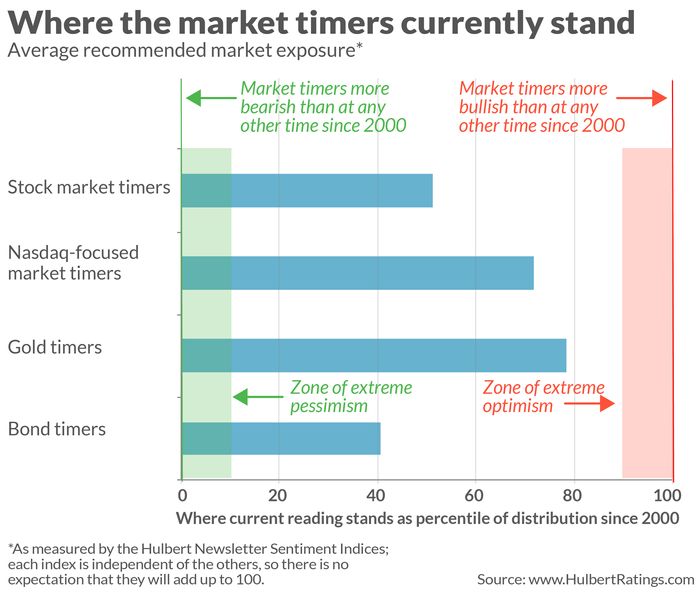

The stock market is just one of the arenas in which my firm tracks market timers’ average exposure levels. My firm also constructs comparable indices that focus on the broad U.S. stock market (as represented by the S&P 500

SPX,

or the Dow), the gold market, and the U.S. bond market. The chart below summarizes where the timers currently stand in all these arenas.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at [email protected]

More: This signal for U.S. stocks bodes well for a rally as some stability returns to the banking sector

Also read: Recession isn’t a guaranteed stock-market crusher, owing to this one truth about volatility and GDP

Read the full article here